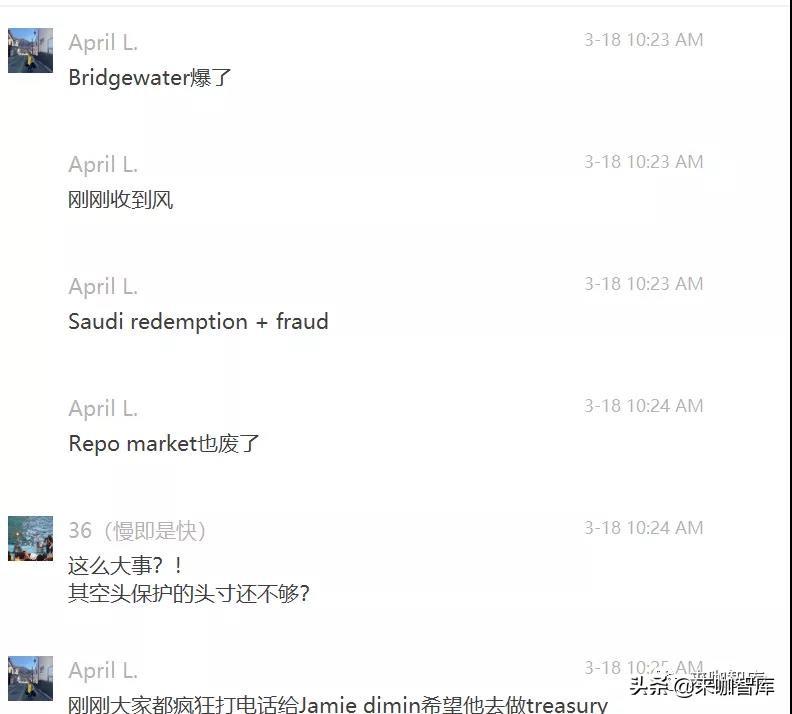

因为全球资本市场近两周的表现堪称几十年难遇,桥水今天公布了一个业绩,它旗下的全天候策略基金(AllWeather)和纯阿尔法策略基金(PureAlpha)3月以来跌幅超近10%-20%。也算是很不好看了。下午,市场中各种分析就冒出来了。

网友A的分析

Just got it from my friend who works at a Hedge Fund

Hope u are well I think we are heading to a total stop in US. This piece is worth your attention...

Guys,

I wanted to share for any input. I’ve been watching what is going on in markets and my conclusion was that Risk Parity has blown up and Citadel and Millennium are in deep trouble. I just received a call from an old GS friend who now runs a large part of a Japanese bank balance sheet in the US and he was highly agitated...

我想分享一下。我一直在观察市场的走势,结论是现在风险平价策略已经崩塌,Citadel和Millennium已深陷困境。我刚接到一个高盛的老朋友(他目前在美国管理一家日资银行的大部分资产负债)打来的电话,他对现状深感焦虑。

His observation is that Bridgewater has faced massive redemptions from Saudi and others and that is what is caused some of the more dramatic moves last week (gold, bonds, equities and FX). He thinks AQR and 2 Sigma are in the same boat. There is massive forced liquidation of risk parity. All of them run leverage in the strategy, sometimes significant. Sovereign wealth, he thinks, is running for the hills as are others.

他看到桥水面临来自沙特和其他投资人的大规模赎回,这也是导致上周一些剧烈震荡(黄金、债券、股票和外汇)的原因。他认为AQR和2 Sigma也面临同样问题。风险平价策略投资组合被大规模强制清算,其中全部都在投资中使用了杠杆,有些还杠杆率惊人。他认为,主权财富基金和其他机构一样也都在逃跑。

My friend explained that due to the Volker rules, now that vol has risen, we has to cut risk limits by 80% in many areas – to put it in perspective his Dollar Mex position limit has gone from 200m to 12m. Thus, just when he was supposed to prove liquidity, he has to reduce it. His hands are tied. Even worse, he has to hedge counterparty risk with corp borrowers and that is adding to the tail spin of selling. There is no liquidity from the banks.

我的朋友解释说,由于沃尔克规则,现在vol已经上涨,使其不得不在许多领域削减80%的风险限额——例如,其美元Mex头寸限额已从2亿美元减至1200万美元。因此,就在他本应提供流动性的时候,却不得不被迫减少流动性。更糟糕的是,他必须对冲公司类借款人的交易对手风险,这进一步加剧了抛售。银行没有能够向市场提供流动性。

The same VAR issue, he claims, is hitting Citadel and Millennium but with a twist. He, along with all the banks, is jacking up lending rates to counterparties from Libor +35 to Libor +90 and he has a $1.5trn balance sheet. The funding stress is forcing banks to reduce lending risk. The issue is that the funding stress is coming from Citadel and Millennium it seems. They rely on repo but via the banks but the transmission mechanism is broken (regulation). It appears that Bernanke probably called Powell and asked him to flood with liquidity at repo but instead of $500bn being drawn, only $78 was drawn. The banks don’t need the cash and don’t want to lend to counterparties. And there in lies the problem – a full credit crunch.

他声称,同样的VAR问题正在冲击Citadel和Millennium,但更复杂。与其他所有的银行一起,他将对手方贷款利率从Libor+35基点提高到Libor+90基点,他的资产负债表为1.5万亿美元。融资压力迫使银行降低自身贷款风险。问题在于,融资压力似乎来自Citadel和Millennium,他们依赖于通过银行回购获得资金,但由于监管的原因,该传导机制被打破了。伯南克可能打电话给鲍威尔,要求美联储通过回购向市场注入大量流动性,但5000亿美元只放出去780亿美元。银行不想借给对方资金,也就不需要资金,因此导致全面的信贷紧缩。

With rates going up, all the relative value trades have blown up. Nothing works any more as they were making 12bps in illiquid stuff on massive leverage (off the runs, etc). As funding goes up they instantly go wildly unprofitable and are stuck either begging for repo funding or having to unwind and realize massive losses. There is no funding. This is big trouble.

随着利率上升,所有的相对价值交易都崩塌了。他们原来通过巨大的杠杆率投资于非流动性资产以赚取12个基点的策略,现在都不管用了。随着融资成本的增加,这些交易立即变得完全无利可图。他们要么苦苦乞求通过回购融资,要么被迫平仓并实现巨额亏损。没有融资渠道是个大麻烦。

These guys are short vol (VAR), short liquidity and short rates. The perfect fucking storm.

这些人在做空vol(VAR),做空流动性,做空利率,这简直是完美风暴。

Then on top of that, my friend who was almost yelling to me about it, says he cannot take any risk and therefore cannot provide liquidity. His hands are tied.

不仅如此,我的朋友几乎对我大喊,说他不能再承担任何风险,因此也就不能再提供流动性。他实在是无能为力了。

COVID makes it even worse and liquidity is going to massively dry up next week and for the next few weeks. You see under Series 24 of FINRA, a trader cannot make markets from home. It is illegal. So everyone is getting sent home but the traders. The problem is the traders are now falling ill – JPM and CS are the two I’ve heard thus far. They will have to go home and each day more do, or decide they want to, the lower liquidity gets. No one can make markets.

冠状病毒使情况更糟。下周和未来几周,流动性将大量枯竭。根据FINRA的Series 24规定,交易员在家里做市是违法的。所以别人都回家了,只有交易员不能回。问题在于,越来越多的交易员们都生病了——我到目前为止听到的有摩根大通和CS两家——他们将不得不回家。随着被迫或决定回家的人越多,市场流动性就越低,因为没有人做市了。

Also, in the corp credit markets things are equally fucked up. Credit, due to the liquidity issues, has stopped trading. That is causing IG etc to blow out. When banks lend to corps, a separate desk (CVA or CPM desk) shorts the stock or buys the CDS etc as a hedge (regulations again) and if the loan is still on the books (they are not allowed to own the bonds but can lend to counterparties, bizarrely) they continues to do that as stocks fall or CDS widens. Essentially, they are short gamma, creating a lob sided market. Everyone is a seller and no one is a buyer. The banks have made money on the hedges while the debt markets get worse.

此外,在公司信用市场,情况也同样糟糕。由于流动性问题,信用市场已经停止交易了。这正在导致IG等陷入困境。又是根据监管要求,当银行向公司放贷时,会有另一个部门(CVA或CPM)做空股票或购买CDS等作为对冲。如果贷款仍在账面上(奇怪的是,他们不可以持有对手方债券,但可以借款给他们),他们在股票下跌或CDS点差扩大时会继续如此操作。本质上,他们在做空gamma,形成单方向市场。每个人都在卖,却没有人买。在债务市场恶化的同时,银行在对冲上可以赚钱。

This is causing the equity value of many firms such as Haliburton, to fall below the debt levels. Whether these borrowers have cash on balance sheet or not is irrelevant because of the falling equity value in this market and from the CVA hedging. That is causing spreads to blow out and it will cause downgrades, thus creating a doom loop.

这导致Haliburton等许多公司的权益价值低于债务水平。因为市场中的股票价值下降和CVA对冲,这些借款人是否在资产负债表有现金都不重要了。这将导致息差扩大,并导致评级下调,从而形成恶性循环。

So, we have a total shit storm if vol stays here for any period of time. I do not see vol falling yet and that is going to cause a really big issue with Citadel, Millennium, all the risk parity unwinds, all the risker credit that is being shorted for hedging and the repo that no one wants in the banks but their counterparties desperately needs. Every day this situation continues, the more dangerous it is going to get....

所以,如果vol持续保持在现有水平,我们会有大麻烦。我认为vol暂时不会下跌,这将对Citadel、Millennium,所有风险平价组合平仓,所有为对冲而做空的高风险信用资产,对手方迫切需要而没有银行愿意做的回购交易等,都造成真正的大问题。这种情况持续的时间越长,就越是危险。

We have a big fucking margin call under way.

我们将会有一大波保证金通知来袭。

In my friends opinion, the only way to stop this is to remove the Volker rule under the emergency powers act ( to allow banks to provide liquidity), the Fed to cut to zero and for them to buy corporate bonds. All the banks have been talking to FINRA and they have said go to the government. Problem is Jamie Dimon is in bed. They need him to run the US Treasury as he is the only person who understands all of this and can navigate it through the politics.

在我的朋友看来,阻止这种情况的唯一办法是取消《紧急权力法》(emergency powers act)下的沃尔克规则(Volker rule),以允许银行提供流动性。联储应将基金利率削减到零,并购买公司债券。所有的银行都和FINRA谈过了,但FINRA说应该去找政府。问题在于杰米·戴蒙(摩根大通CEO)还生病在床。应该由他来管理美国财政部,因为他是唯一了解全局,并有能力驾驭政治的人。

This is likely the fix that needs to happen. What happens to Citadel, Millennium, Bridgewater, AQR, 2 Sigma and the corp bond market until they pull that trigger, I have no idea.

这可能是必要的解决问题的办法。在此之前,Citadel,Millennium,Bridgewater,AQR,2 Sigma和公司债券市场会发生什么,我不知道。

I thought you’d all be interested.

我猜你们会对以上这些感兴趣。

网友B的分析

让人更为吃惊的是,上周仍然处于平静状态的回购市场,周一突然“疫情”发作,回购利率跳升到了2%!要知道美联储已经将联邦基准利率降到了0附近,超额准备金利率(IOER)也降到了0.1%,回购利率应该低于超额准备金利率,否则,银行坐拥的1.3万亿美元的超额准备金,应该立刻从美联储账户中涌向回购市场进行套利,从而将回购利率压下来。与去年9年美国爆发钱荒时发生的现象一模一样。银行“断然拒绝”了这个“无风险”套利的机会。

所谓无风险,是指回购市场以国债为抵押进行隔夜融资,抵押品非常可靠,时间只有一晚,比银行之间无抵押的纯信用借贷更靠谱。

银行放弃赚钱的好机会只有两个可能,一是不敢,二是不能。

先说为什么不敢。上周以桥水基金的达里奥为代表的风险平价型对冲基金(Risk Parity funds)大暴雷,很多对冲基金用十倍以上的杠杆管理着数万亿美元的资产,他们完全没有预料到三四个标准方差以上的黑天鹅们正在逼近,特别是石油和病毒这对“黑风双煞”的杀伤力如此惊人,远远超过了他们的想象。

风险平价策略的“祖师爷”达里奥在今年一月时还曾信心满满,他在达沃斯论坛中放出狂言“Cash is trash!”(现金就是垃圾!),号召投资人在2020年的市场上“胆子更大一些,步子更快一些”,冲向全球市场,拥抱多样化的资产,千万不能持有现金。

“祖师爷”的总动员,激发出全球风险平价型对冲基金经理们的狂热,他们积极招募客户,放胆配置资产。

美国国债就是他们的最爱,大举吃进之后,反手就在回购市场上质押融资,然后再买国债,再进行回购融资,以循环抵押的方式做大资产规模。

事实上,当中国、日本、沙特等美国国债大买主逐渐丧失了对美债的胃口之后,高倍杠杆的对冲基金一跃成为美国国债最重要的新买家,在前两年美联储加息缩表卖出国债时,正是对冲基金们承担起“为国接盘”的重任,成功地压制了国债收益率的上涨势头。

当达里奥们在上周被“黑风双煞”彻底打垮之后,高杠杆成了“索命鬼”,迫使他们启动了疯狂的国债抛售模式,在3月11日终于导致美国国债市场丧失了流动性,一级交易商们的自有资金已难以应付对冲基金的大溃败,被迫向美联储求救,这才有了3月12日美联储紧急开始的1.5万亿回购注入资金的救命行动。

从3月16日本周一开始,对冲基金的雪崩态势终于开始冲击美国金融体系的心脏—回购市场。在这种风声鹤唳的情况下,哪家银行敢于借钱给这些“残兵败将”?

对冲基金手中的用于回购融资的国债,背后平均有三个主人,这种“一女三嫁”的回购抵押品,谁敢接手?银行也是聪明人,为了区区2%的套利,却冒着赔掉本金的风险,这买卖没人愿意干!

还有另一种情况,银行的1.3万亿超额准备金根本就无法动用。为什么?对冲基金也好,影子银行也罢,所有资金的源头都在银行,银行“清白”的资产负债表与影子银行的“黑暗交易”存在着千丝万缕的联系。

如果大批对冲基金破产,银行岂能独善其身?简单地说,地主家也没有余粮了。怎么办?还得美联储出手拯救。3月16日周一,美联储急急忙忙地宣布下午1:30分,再一次向市场注入5000亿美元的回购资金,目的是为了“确保准备金供应充足,以支持短期资金市场(国债回购)的正常运行”。

说白了,对冲基金玩砸了要跳楼甩卖国债,最终还是要美联储印钞票接盘。

上周美联储刚搞了1.5万亿的回购,这周又追加5000亿,再加7000亿的QE,达里奥们究竟玩砸了多大规模的资产?又会有多少交易对手将被这帮人拖下水?银行、保险公司、共同基金、养老基金可都是达里奥们的金主。

美联储一连串的高强度救援,反而印证了市场的猜疑,加剧了市场恐慌。

针对这一众说纷纭的事件,来咖周围的吃瓜群众也纷纷表态:

来咖吃瓜群众A

“millennium的同学说,我们之前投资期改五年了,不会大批redemption。但是现在市场这样,估计performance不会很好。”

来咖吃瓜群众B

“如果是真的那就麻烦了。因为美国的货币政策已经到底了,杠杆的东西有多大的窟窿真的不知道,按理说美联储或者说是就华尔街的这帮人,他们其实心里应该有个数,做多少倍的杠杆对应多少倍的资产。就是十个锅九个盖子或者八个盖子,怎么样能盖得过来,他会算好的。

但是要照这么说的话,就是一连串的反应,像桥水这种这么大的基金都爆雷的话。那就等于是华尔街整个头寸管理失败了。那这样的情况下,后面杠杆加杠杆,会带来多少雷是根本不知道的,就是你刚算出来可能不大,但是未来的延续性会很长,积累的雷会很大。”

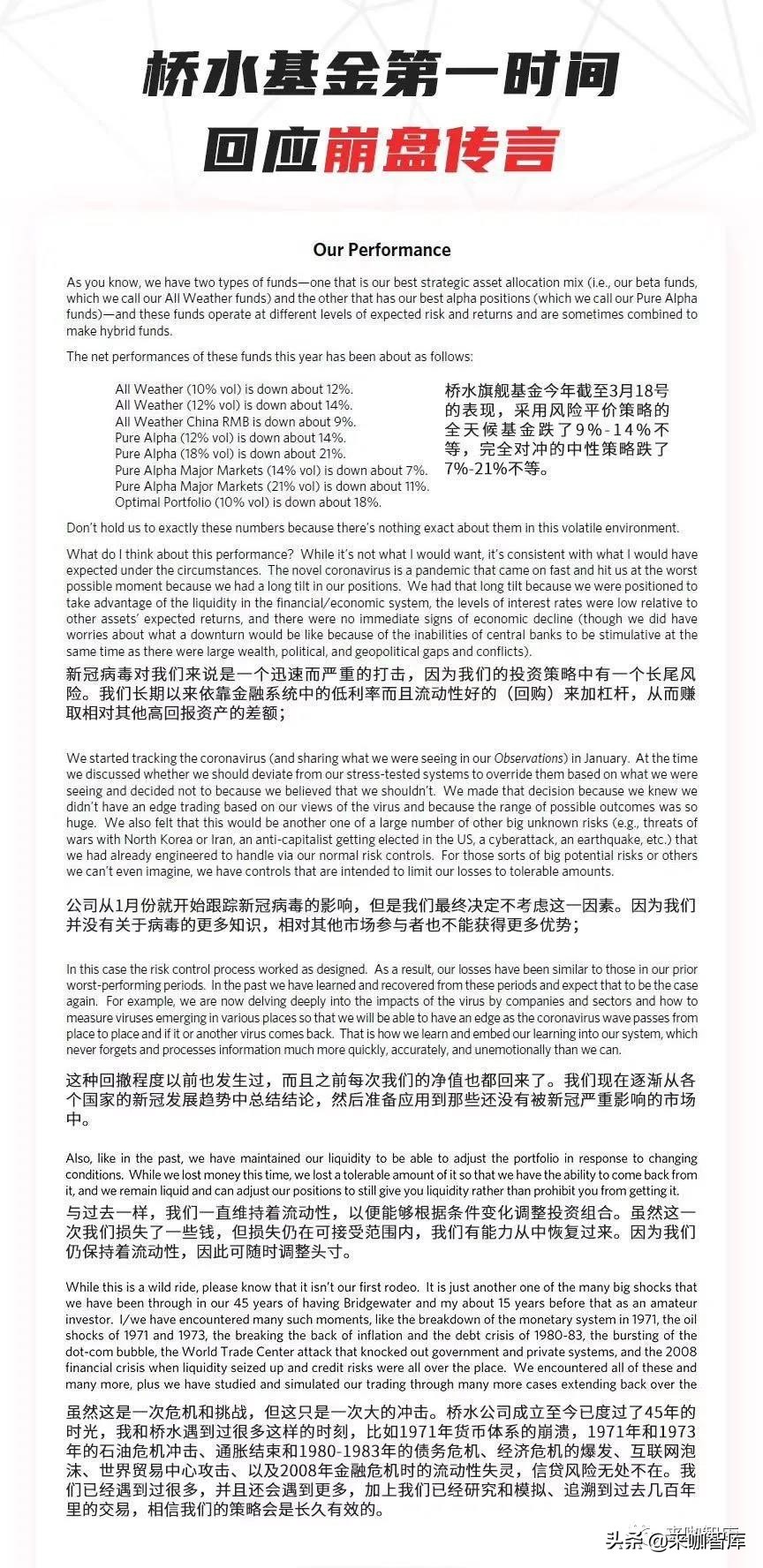

不过,小编认真仔细看了看,这个公开的“晒单”也并不能作为是否爆仓的直接回应,截至发稿,桥水官方并没有对“爆仓”一事做出直接正面回应。今晚的美股,拭目以待了。

版权声明:CosMeDna所有作品(图文、音视频)均由用户自行上传分享,仅供网友学习交流。若您的权利被侵害,请联系删除!

本文链接://www.cosmedna.com/article/214147847.html